Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Financing Contingency: Making Sense of the Written Statement Options

When you’re filling out the financing contingency section of the Minnesota Purchase Agreement, do the written statement options feel clear as mud? Let’s break it down simply.

First, choose either Line 70 or Line 77 — not both.

Option 1: Lines 70–73

This gives the buyer until closing to secure financing. If financing falls through, the agreement is canceled and the earnest money is either:

- Refunded to Buyer (most buyer-friendly), or

- Retained by Seller (adds consequence if buyer doesn’t perform).

This option gives the buyer the most flexibility.

Option 2: Lines 77–112

This requires the buyer to provide a written statement from their lender by a specific date before closing. This gives the seller peace of mind earlier in the process.

- Talk to your lender to choose a realistic date for the written statement.

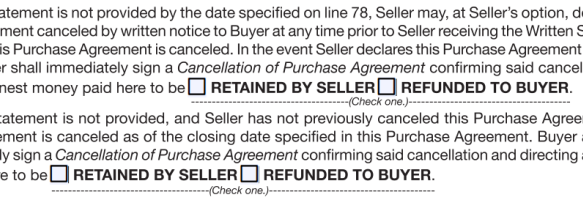

What if the Written Statement Isn’t Provided?

Lines 104–108

If the buyer misses the written statement deadline, the seller can cancel the agreement. Then, decide what happens to the earnest money:

- Retained by Seller: Strongest protection for the seller.

- Refunded to Buyer: Neutral choice, especially if the buyer’s situation changed unexpectedly (e.g., job loss).

Lines 109–112

If the seller doesn’t cancel and waits until closing, but financing still falls through, the agreement is automatically canceled. Then:

- Retained by Seller: Recognizes the seller’s time and expenses.

- Refunded to Buyer: More buyer-friendly, but less common if the seller has been accommodating.

Bottom Line forAgents:

- Buyers: Choose the option that gives your buyer enough time and aligns with the lender’s timeline.

- Sellers: Protect their interests by understanding when and how they can cancel — and what happens to the earnest money.